Více o knize

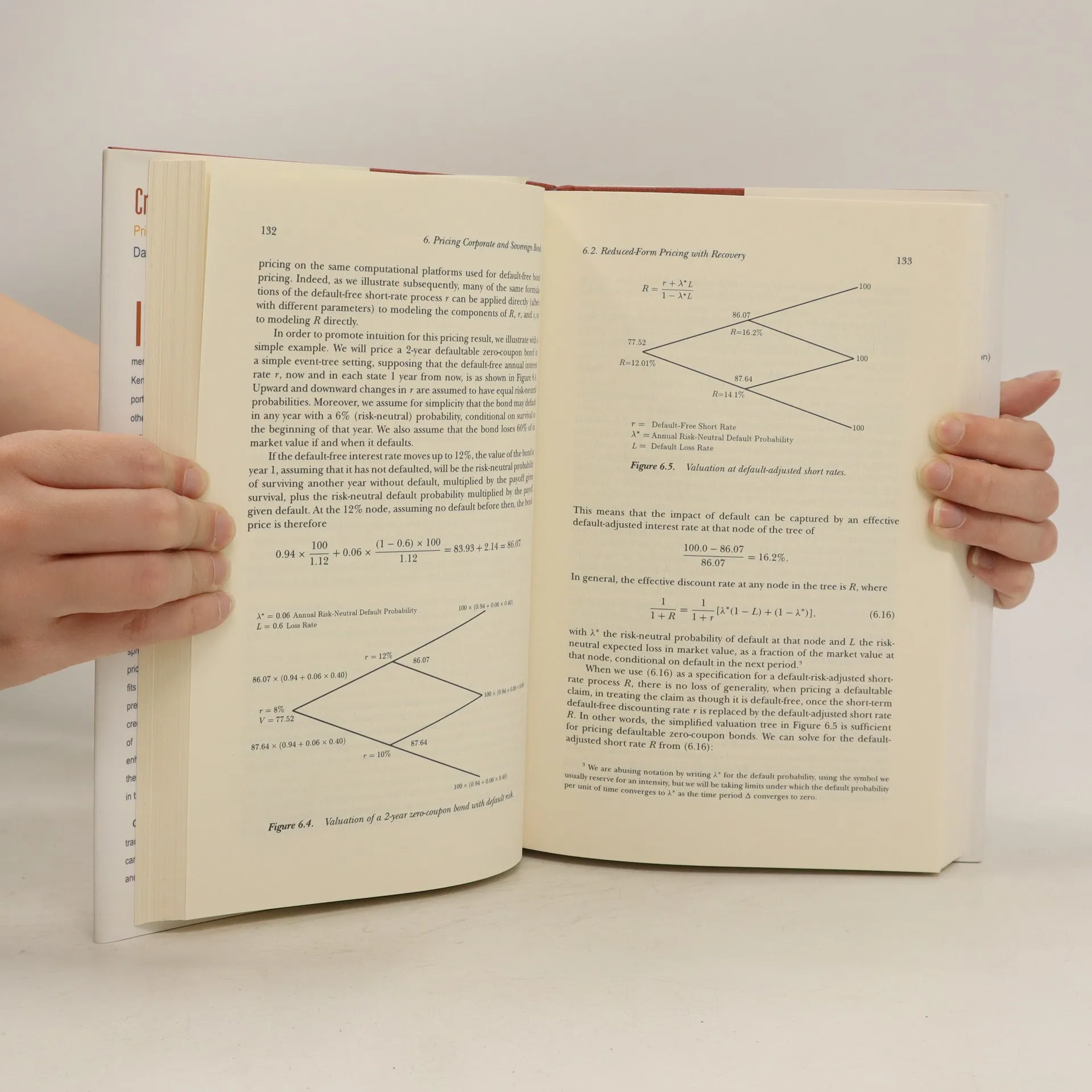

In this book, two leading economists offer a comprehensive exploration of the foundations for credit risk pricing and measurement. Darrell Duffie and Kenneth Singleton adeptly model credit risk to assess portfolio risk and price defaultable bonds, credit derivatives, and other securities subject to credit risk. Their rigorous and sophisticated analysis provides an unparalleled examination of pricing and credit derivatives, addressing a critical issue as financial institutions globally refine their credit management strategies. The authors critically evaluate various credit-risk modeling approaches, discussing their strengths and weaknesses. They combine theoretical insights with extensive empirical analyses of credit-related time series, including default probabilities, recoveries, ratings transitions, and yield spreads. Both "structural" and "reduced-form" methods for pricing defaultable securities are presented, with assessments of their historical data fits. The book also covers the pricing of credit derivatives such as credit swaps, collateralized debt obligations, credit guarantees, lines of credit, and spread options. Furthermore, the authors suggest enhancements to current pricing and management practices to better equip financial institutions for future market changes. This resource is essential for risk managers, traders, regulators, academic researchers, and students engaged with financial products carrying significa

Nákup knihy

Credit Risk, Darrell Duffie, Kenneth J. Singleton

- Jazyk

- Rok vydání

- 2003

- product-detail.submit-box.info.binding

- (pevná)

Doručení

Platební metody

Tady nám chybí tvá recenze.

- Titul

- Credit Risk

- Jazyk

- anglicky

- Vydavatel

- Princeton University Press

- Rok vydání

- 2003

- Vazba

- pevná

- Počet stran

- 464

- ISBN10

- 0691090467

- ISBN13

- 9780691090467

- Série

- Hodnocení

- 2,6 z 5

- Anotace

- In this book, two leading economists offer a comprehensive exploration of the foundations for credit risk pricing and measurement. Darrell Duffie and Kenneth Singleton adeptly model credit risk to assess portfolio risk and price defaultable bonds, credit derivatives, and other securities subject to credit risk. Their rigorous and sophisticated analysis provides an unparalleled examination of pricing and credit derivatives, addressing a critical issue as financial institutions globally refine their credit management strategies. The authors critically evaluate various credit-risk modeling approaches, discussing their strengths and weaknesses. They combine theoretical insights with extensive empirical analyses of credit-related time series, including default probabilities, recoveries, ratings transitions, and yield spreads. Both "structural" and "reduced-form" methods for pricing defaultable securities are presented, with assessments of their historical data fits. The book also covers the pricing of credit derivatives such as credit swaps, collateralized debt obligations, credit guarantees, lines of credit, and spread options. Furthermore, the authors suggest enhancements to current pricing and management practices to better equip financial institutions for future market changes. This resource is essential for risk managers, traders, regulators, academic researchers, and students engaged with financial products carrying significa