Parametry

Kategorie

Více o knize

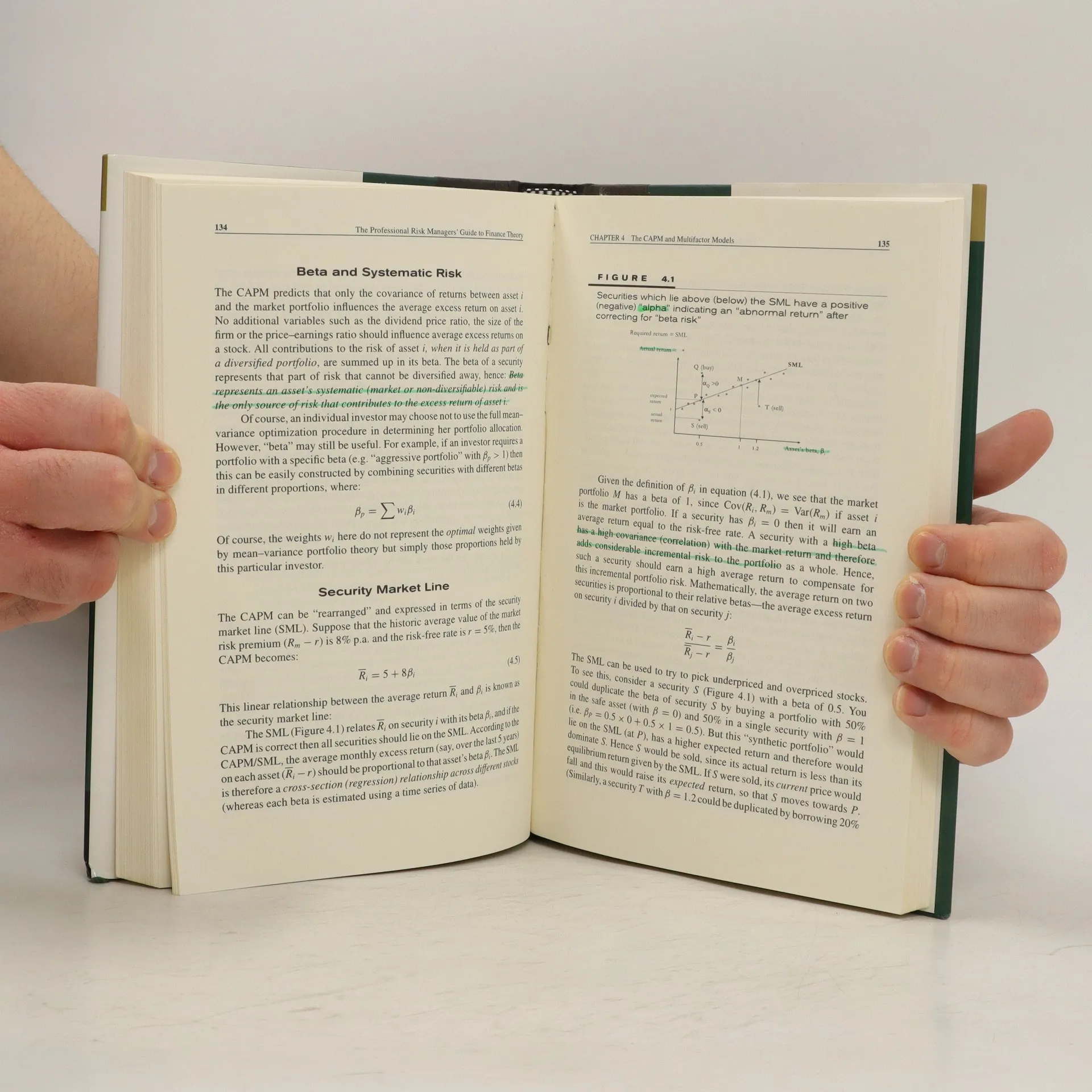

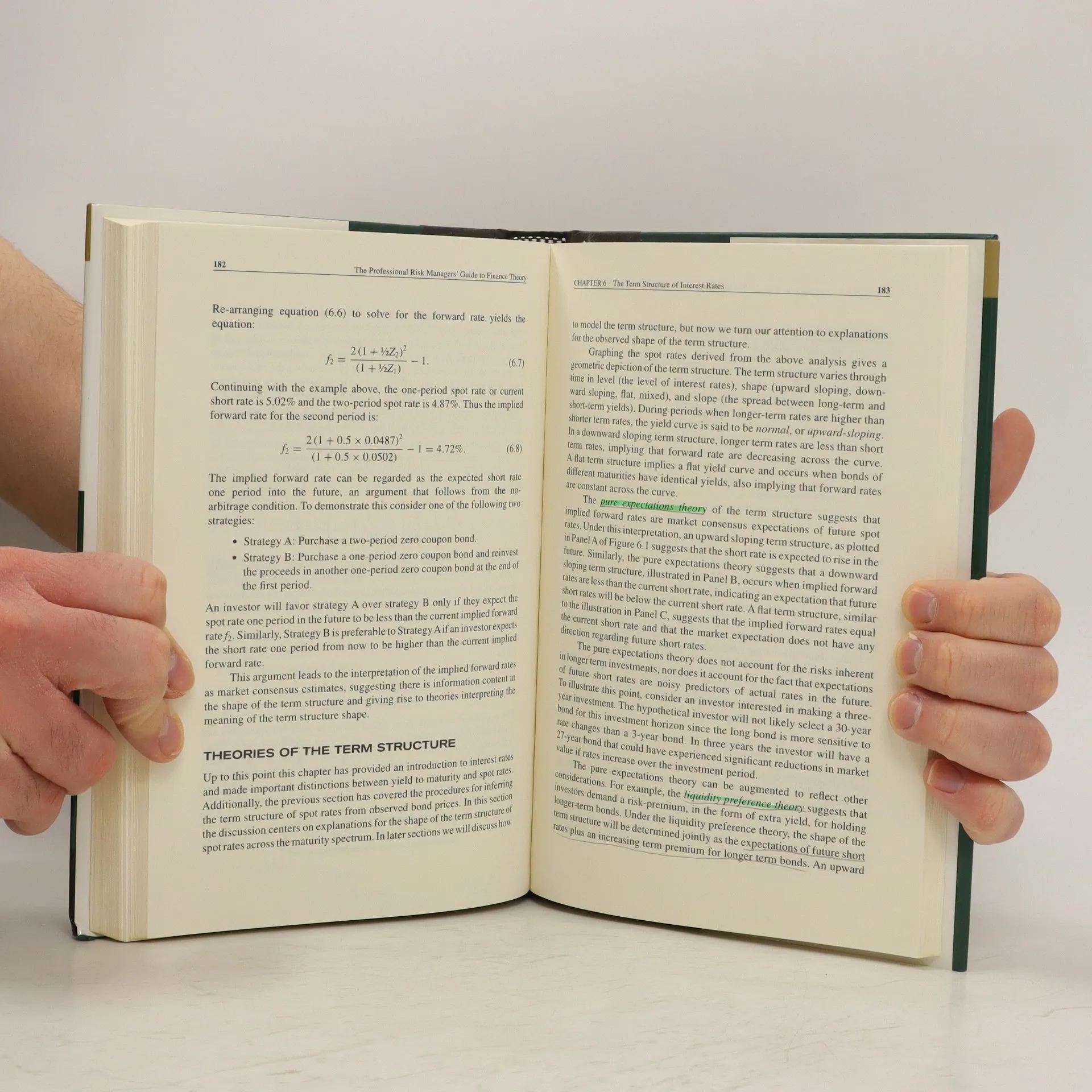

This comprehensive reference brings together ten of the worlds leading scholars and practitioners, who provide invaluable perspectives on all aspects of finance theory and how they are applied to the process of risk management. The book begins with an overview of risk and risk aversion, introducing utility functions and the mean-variance criterion. It then delivers a thorough introduction to portfolio mathematics, including discussion of the efficient frontier, portfolio theory, and portfolio diversification. Written to help you fortify your defenses against extreme, unanticipated outcomes, and to ensure that returns are an adequate reward for risks taken, The Professional Risk Managers Guide to Finance Theory and Application covers key issues such as: The theory of capital allocation Capital structure, that is, debt versus equity financing The CAPM and multifactor models Interest rate models The term structure of interest rates No-arbitrage pricing of futures and forwards Risk-neutral valuation of options Offering a global view not found elsewhere, The Professional Risk Managers Guide to Finance Theory and Application arms institutional investors, professional financial analysts and traders, auditors, corporate treasurers, regulators and actuaries with the practical tools to master any financial field.

Nákup knihy

The Professional Risk Managers Guide to Finance Theory and Application, Kolektiv

- Vpisky / podtrhávání

- Jazyk

- Rok vydání

- 2007

- product-detail.submit-box.info.binding

- (pevná s přebalem)

Doručení

Platební metody

Navrhnout úpravu

- Titul

- The Professional Risk Managers Guide to Finance Theory and Application

- Jazyk

- anglicky

- Autoři

- Kolektiv

- Vydavatel

- Mcgraw-hill

- Rok vydání

- 2007

- Vazba

- pevná s přebalem

- ISBN10

- 0071546472

- ISBN13

- 9780071546478

- Kategorie

- Podnikání a ekonomie

- Anotace

- This comprehensive reference brings together ten of the worlds leading scholars and practitioners, who provide invaluable perspectives on all aspects of finance theory and how they are applied to the process of risk management. The book begins with an overview of risk and risk aversion, introducing utility functions and the mean-variance criterion. It then delivers a thorough introduction to portfolio mathematics, including discussion of the efficient frontier, portfolio theory, and portfolio diversification. Written to help you fortify your defenses against extreme, unanticipated outcomes, and to ensure that returns are an adequate reward for risks taken, The Professional Risk Managers Guide to Finance Theory and Application covers key issues such as: The theory of capital allocation Capital structure, that is, debt versus equity financing The CAPM and multifactor models Interest rate models The term structure of interest rates No-arbitrage pricing of futures and forwards Risk-neutral valuation of options Offering a global view not found elsewhere, The Professional Risk Managers Guide to Finance Theory and Application arms institutional investors, professional financial analysts and traders, auditors, corporate treasurers, regulators and actuaries with the practical tools to master any financial field.