Miláček čtenářů je právě vyprodaný

Parametry

- 544 stránek

- 20 hodin čtení

Více o knize

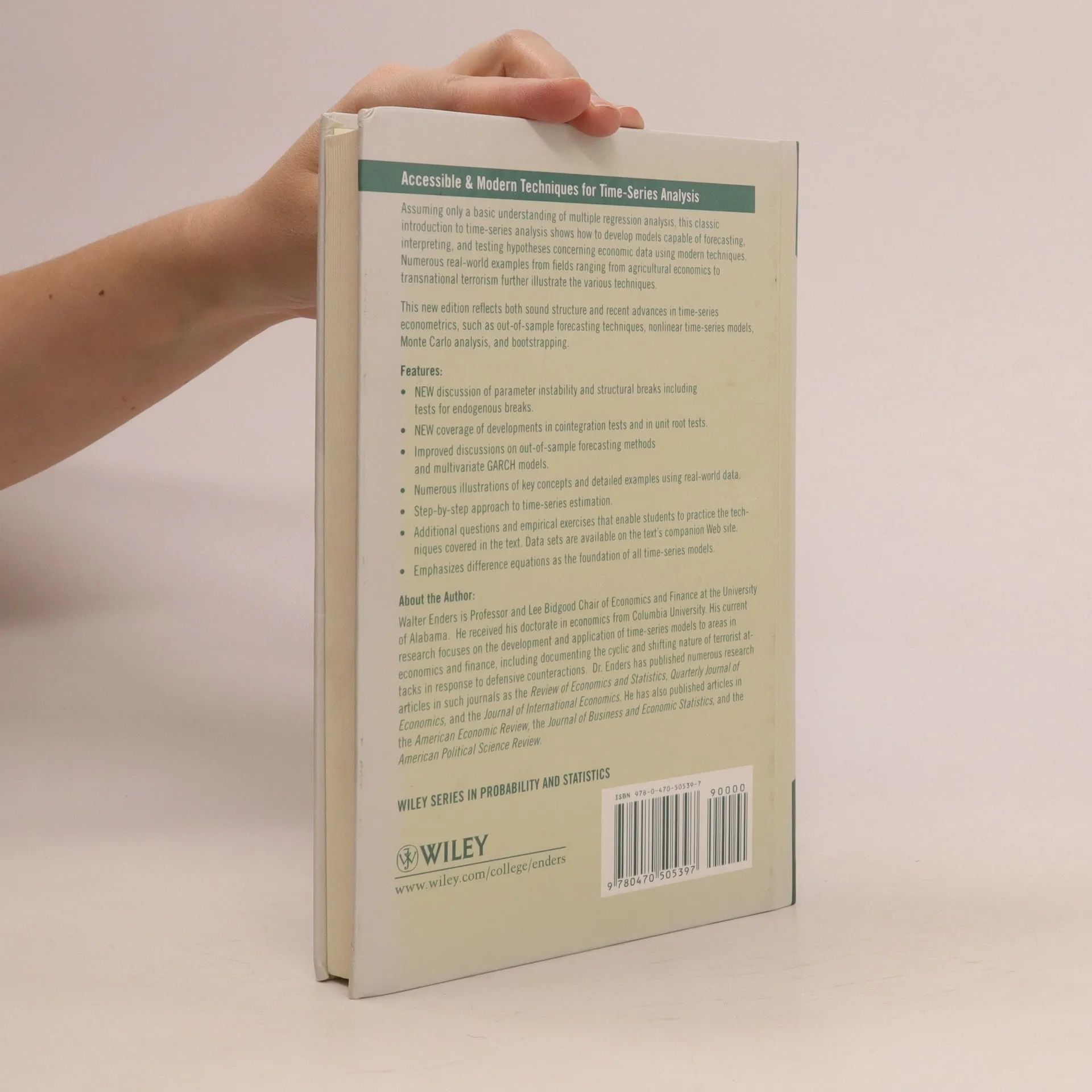

Enders continues to provide business professionals with an accessible introduction to time-series analysis. He clearly shows them how to develop models capable of forecasting, interpreting, and testing hypotheses concerning economic data using the latest techniques. The third edition includes new discussions on parameter instability and structural breaks as well as out-of-sample forecasting methods. New developments in unit root test and cointegration tests are covered. Multivariate GARCH models are also presented. In addition, several statistical examples have been updated with real-world data to help business professionals understand the relevance of the material.

Nákup knihy

Applied Econometric Time Series, Walter Enders

- Jazyk

- Rok vydání

- 2010

- product-detail.submit-box.info.binding

- (pevná)

Jakmile se objeví, pošleme e-mail.

Doručení

Platební metody

Tady nám chybí tvá recenze.

- Titul

- Applied Econometric Time Series

- Jazyk

- anglicky

- Autoři

- Walter Enders

- Vydavatel

- Wiley

- Rok vydání

- 2010

- Vazba

- pevná

- Počet stran

- 544

- ISBN10

- 0470505397

- ISBN13

- 9780470505397

- Série

- Hodnocení

- 3,65 z 5

- Anotace

- Enders continues to provide business professionals with an accessible introduction to time-series analysis. He clearly shows them how to develop models capable of forecasting, interpreting, and testing hypotheses concerning economic data using the latest techniques. The third edition includes new discussions on parameter instability and structural breaks as well as out-of-sample forecasting methods. New developments in unit root test and cointegration tests are covered. Multivariate GARCH models are also presented. In addition, several statistical examples have been updated with real-world data to help business professionals understand the relevance of the material.