Miláček čtenářů je právě vyprodaný

Parametry

- 692 stránek

- 25 hodin čtení

Více o knize

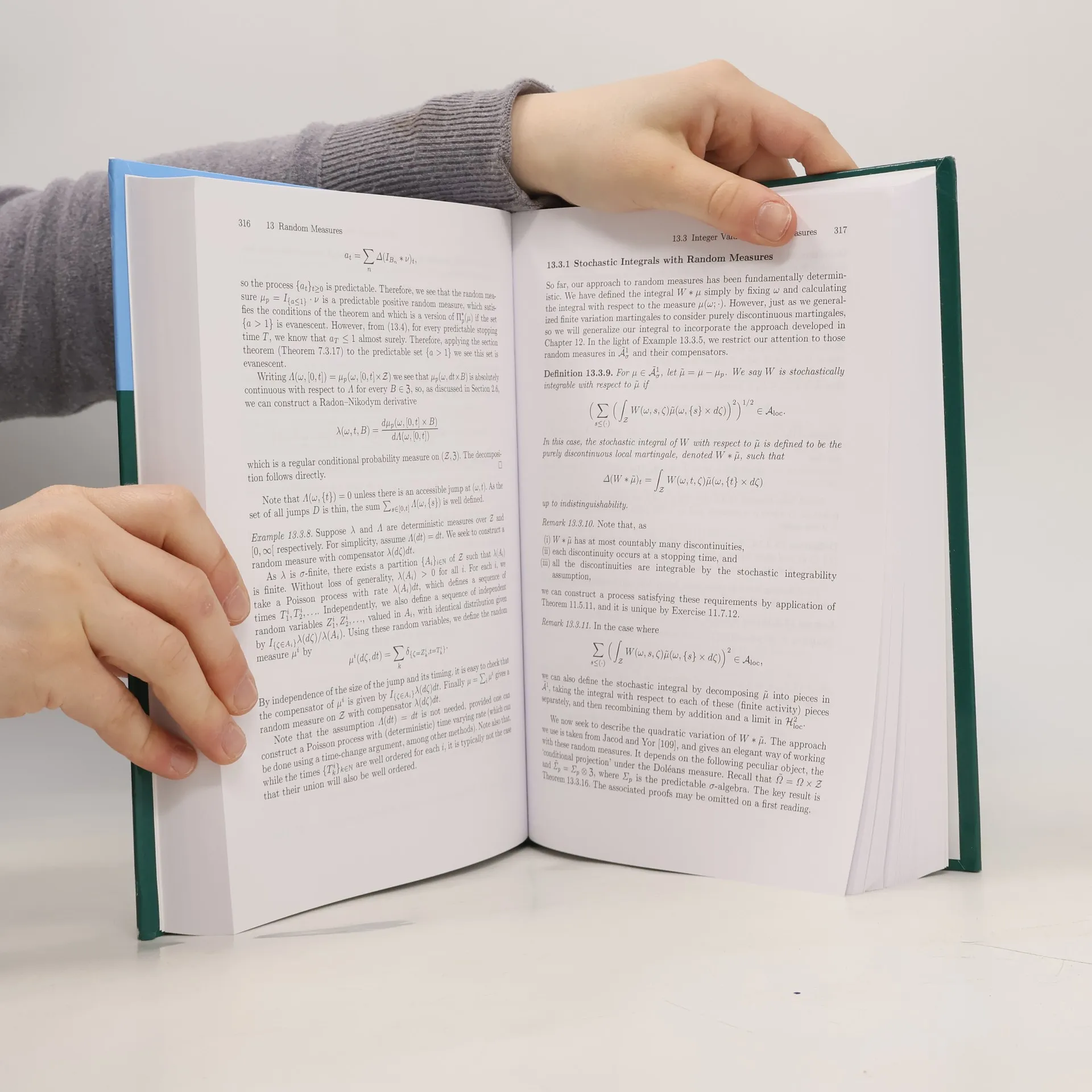

The revised edition offers an in-depth exploration of modern random processes and stochastic integrals, catering to readers familiar with basic analysis. It serves as a comprehensive resource for systems theorists, electronic engineers, and professionals in quantitative finance. Expanding on its predecessor, the text is particularly valuable for research mathematicians and graduate students, as well as quantitative analysts in the finance sector, providing essential insights into contemporary applications.

Nákup knihy

Stochastic Calculus and Applications, Samuel N. Cohen, Robert Elliott

- Jazyk

- Rok vydání

- 2015

- product-detail.submit-box.info.binding

- (pevná)

Jakmile se objeví, pošleme e-mail.

Doručení

Platební metody

Tady nám chybí tvá recenze.

- Titul

- Stochastic Calculus and Applications

- Jazyk

- anglicky

- Autoři

- Samuel N. Cohen, Robert Elliott

- Vydavatel

- Springer New York

- Rok vydání

- 2015

- Vazba

- pevná

- Počet stran

- 692

- ISBN13

- 9781493928668

- Série

- Štítky

- Naučná literatura, Byznys, Byznys & Management, Technologie & Průmysl, Věda & Matematika, Matematika, Elektronika & Elektrotechnika

- Hodnocení

- 4 z 5

- Anotace

- The revised edition offers an in-depth exploration of modern random processes and stochastic integrals, catering to readers familiar with basic analysis. It serves as a comprehensive resource for systems theorists, electronic engineers, and professionals in quantitative finance. Expanding on its predecessor, the text is particularly valuable for research mathematicians and graduate students, as well as quantitative analysts in the finance sector, providing essential insights into contemporary applications.